FEATURED RESEARCH – The future of AI in PropTech: Where demand is creating investment opportunity

FEATURED RESEARCH – The future of AI in PropTech: Where demand is creating investment opportunity

The demand for AI in real estate is rising

AI may be overhyped at the moment, but we can confidently say that the direction is clear: Demand for AI-driven solutions in real estate is rising.

According to JLL’s Future of Work Survey 2024, 90.1% of companies plan to run their corporate real estate function with AI and technology supporting human experts. Though understanding of the technology remains low, adoption is gaining momentum, with 61% of companies already piloting different CRE AI use cases.

This research article examines the current PropTech AI provider landscape in relation to the demand for AI in real estate, identifying opportunities and competitive advantages for PropTech companies.

AI-powered PropTech: a young yet steadily growing market

AI is emerging as an area of investment within the global PropTech market. Among 7,000 global PropTech companies, about 10% (700 companies) are currently providing AI-powered solutions, including both AI native products and AI-augmented products.

- AI-native products are designed from the outset with AI as an integral component of their functionality and purpose

- AI-augmented products are originally designed without AI, but later enhanced with AI capabilities to improve functionality or performance. (With the development of GenAI and LLMs, many companies are currently considering this approach.)

When comparing these products to traditional PropTech services, AI’s role can be characterized in four key ways:

- Core capabilities: Foundational AI capabilities that make the product possible, such as image recognition and generation.

- Enhanced analytics: Enhanced analytics and data modeling capabilities, such as more accurate time series predictions.

- New user interfaces: New interface for interaction, for example, instead of dashboards, use chat-based interfaces for data and insight queries.

- Automated processes: Automate highly repetitive and mundane tasks, such as data entry and standardization.

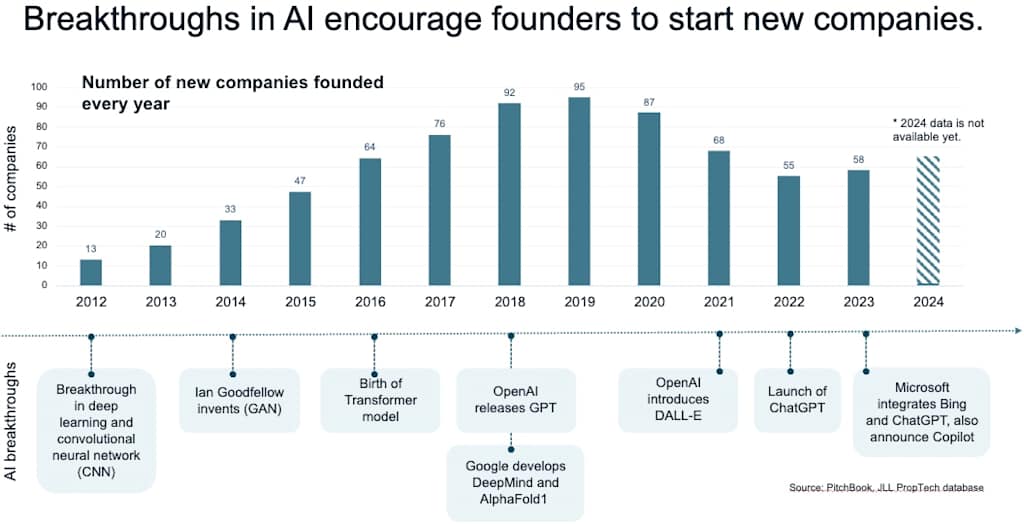

Businesses driven by technology breakthroughs: Advancements in AI technology development have been the driving force behind the emergence of AI-powered PropTech companies, as new foundation models, capabilities and infrastructure become available. Most of these PropTech AI companies were founded after 2012, with two distinct peaks in numbers of companies: one around 2019 in line with breakthroughs in deep learning, and another around 2023 with the release of Generative AI and LLMs.

Market growth is further spurred by declining costs associated with using foundation models, which has lowered barriers to building AI-powered applications. Many PropTech AI companies have shifted their research and development focus from independently training their own models to integrating and optimizing various preexisting models for improved performance.

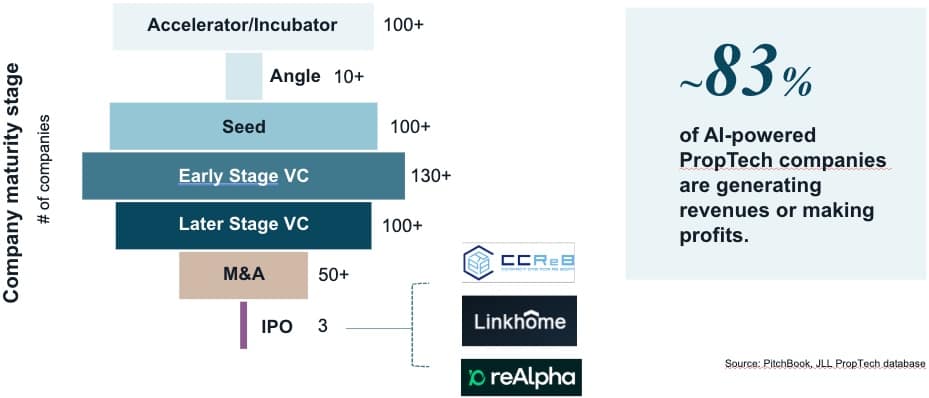

Venture capital as the backbone for development: Venture capital is the biggest source of funding for AI-powered PropTech, with around 62% of companies currently VC-backed. The total VC invested has been steady since 2018, with a peak around 2021 and 2022 due a rise in merger and acquisition deals. Most of the funding deals brokered in the last five years are in their seed round. Only a small proportion (under 8%) of VC-backed AI-powered PropTech companies have reached exits. However, most (83%) are generating revenues or making profits, signaling long-term potential for the market.

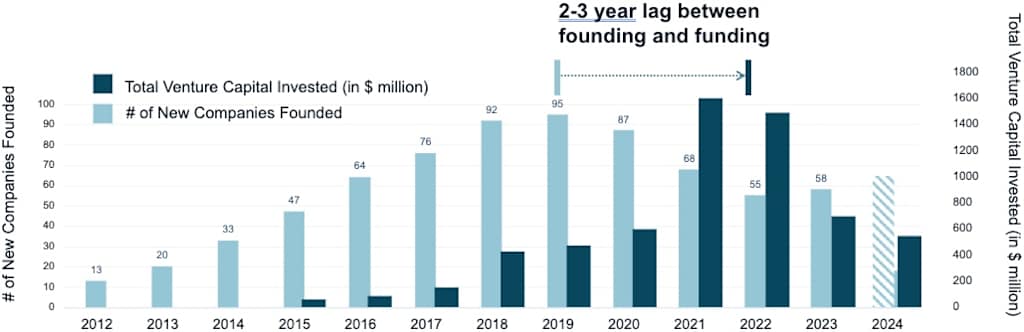

2025 and 2026 outlook: By comparing the number of new companies founded annually and the total amount of venture capital invested, a lag of two to three years is observed between peak company founding and peak capital investment. Based on the number of companies founded in 2023 and 2024, we could expect investment in the next few years to remain strong and steady until picking up when exits start happening.

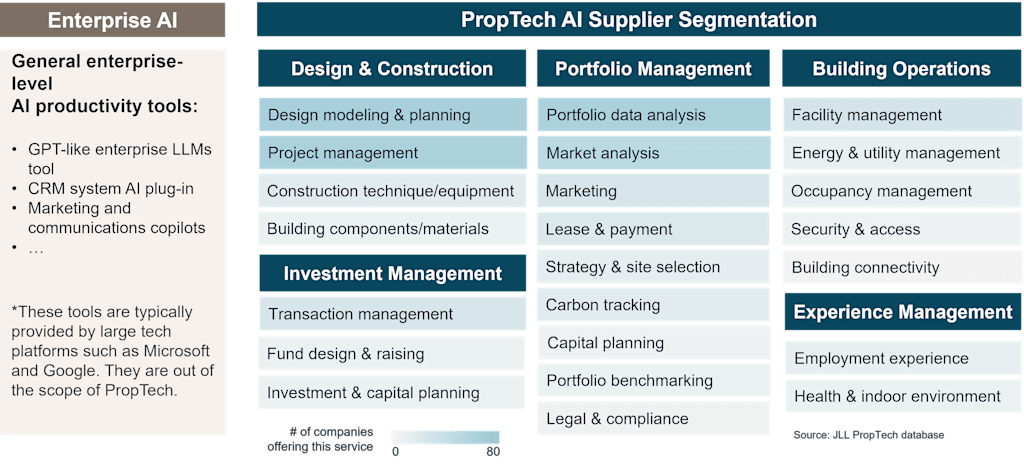

PropTech AI investment opportunities: where demand outpaces supply

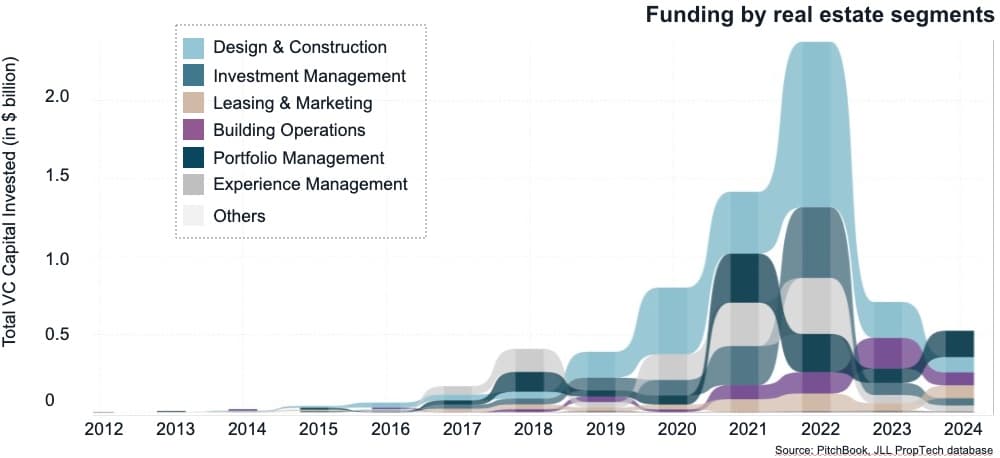

VC investment focus varies by year, driving product development in different real estate segments including design and construction, investment management, portfolio management, building operations and experience management.

Within these categories, there are specific sub-segments where PropTech startups are providing services. Currently, the sub-segments with the most product options are

- Design modelling and planning

- Project management

- Portfolio data analysis

- Market analysis

In comparison, other sub-segments have limited product offerings.

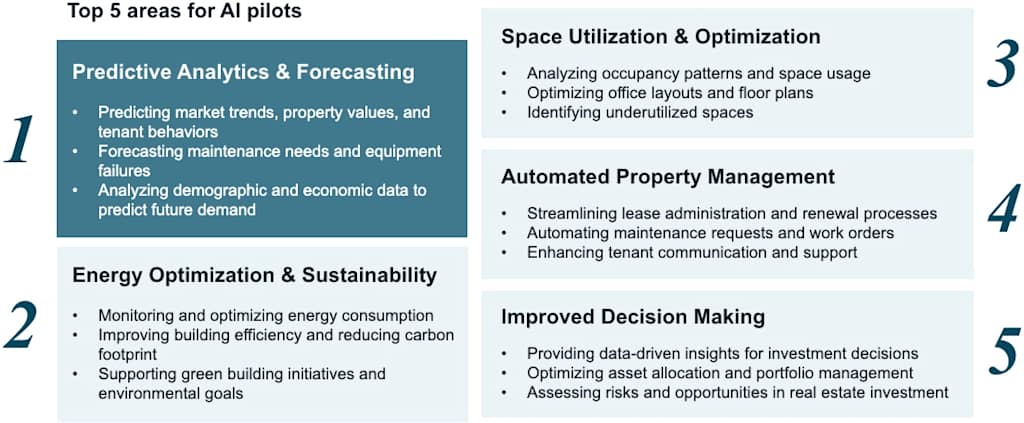

However, JLL’s future of work survey found that companies are piloting AI solutions that extend beyond the top four sub-segments. There are considerable gaps between the AI use cases being piloted by businesses from the demand side, and the current focus of AI PropTech development on the supply side. Predictive analytics represent the only area of overlap between supply and demand, while the other areas lack product options.

In addition to the top five AI pilot areas, there are several emerging areas of interest for CRE users:

- Personalized tenant/employee experience based on preferences

- Enhancing smart security systems and assess control

- Monitor potential hazards and improving disaster response and preparedness

- Optimizing resource allocation and procurement in facilities management to reduce cost

- Developing digital twins for real-time monitoring and optimization

These supply-demand gaps present opportunities for new investments and product development. CRE users expect AI to provide unprecedented insights, automate repetitive tasks and streamline fragmented processes. Crucially, AI tools must address challenges that traditional tech can’t solve or enhance performance with greater efficiency or reduced cost. These user expectations can guide roadmaps for product development in areas where demand outpaces supply.

It is worth noting that PropTech is focused mostly on real estate specific point solutions. Enterprise-level general AI productivity tools and platforms lie outside the scope of PropTech, and is a market dominated by large tech providers such as Microsoft and Google.

Client insights for start-up go-to-market strategies

In JLL’s PropTech study, 100% of AI startups interviewed believe that users prioritize problem-solving capabilities rather than the presence of AI in a product. Understanding user mindsets as well as the current stage of real estate AI adoption can help unlock unique competitive advantages in product design and business strategies.

Several key characteristics define how real estate users currently engage with AI:

- Limited understanding: Despite confidence in AI’s potential, most real estate users lack a sophisticated understanding of how to effectively implement AI within their organizations. Most companies still lack a comprehensive and unified AI strategy for real estate.

- Pressure on ROI: Challenges related to managing costs and navigating a dynamic economic environment leave companies less patient for ROI on AI investments to be realized.

- Adoption barriers: The most significant challenges reported by users include the cost of implementation, data quality and availability, and risks associated with data security and cybersecurity.

- Multi-stakeholder procurement process: Decisions on real estate technology adoption involve not only CRE professionals, but cross-functional stakeholders including IT, HR, finance and others, adding complexity to procurement processes.

Correspondingly, successfully demonstrating the following capabilities in alignment with user needs and expectations could result in competitive advantages.

- ROI delivery: Delivering both immediate and long-term ROI can support the business case for budget allocation.

- Cross-functional value: Supporting CRE professionals in articulating the value of AI solutions for other business functions supports decision-making.

- Collaborative customization: The ability to work with users to customize or partially customize solutions addresses unique business situations

- Data support: Accommodating data deficiencies and offering data generation options to overcome common challenges

- User-friendliness: Intuitive onboarding and interfaces to minimize technical skill required

- Integration with existing systems: Compatibility with corporate IT frameworks to support change management toward AI-powered workflows. Avoiding redundancies with existing tech solutions improves added value

- Strict compliance: Rigorous compliance and protocols to minimize data and cybersecurity risks

End Note

The AI-powered PropTech market is an evolving ecosystem where tech providers and users need to collaborate for growth. Aligning investment and development strategies with the priorities of CRE occupiers and investors can unlock competitive advantage and opportunities to meet market demand. PropTech providers who address user needs and challenges support CRE professionals in establishing the business case for implementing AI.

Written by Yuehan Wang, JLL Global Research

For more PropTech insights, subscribe to our newsletter Spark Notes.

Interested in a strategic partnership with JLL Spark? Apply for an investment here.