FEATURED RESEARCH – Is the tipping point for robotics in real estate coming? The rediscovery of robotics as physical AI

FEATURED RESEARCH – Is the tipping point for robotics in real estate coming? The rediscovery of robotics as physical AI

In 2025, robotics in real estate experienced a renaissance driven by artificial intelligence breakthroughs.

Key Takeaways:

- Physical AI, orchestration, and service-based models are advancing robotics, increasing feasibility and offering better ROI

- Robotics are now on the market to assist with CRE: construction, operations, infrastructure inspections, cleaning & maintenance, and security

- We anticipate the spill over from VC investment in consumer, logistics, and security to push forward CRE robotics development

Historically slow adoption in commercial real estate

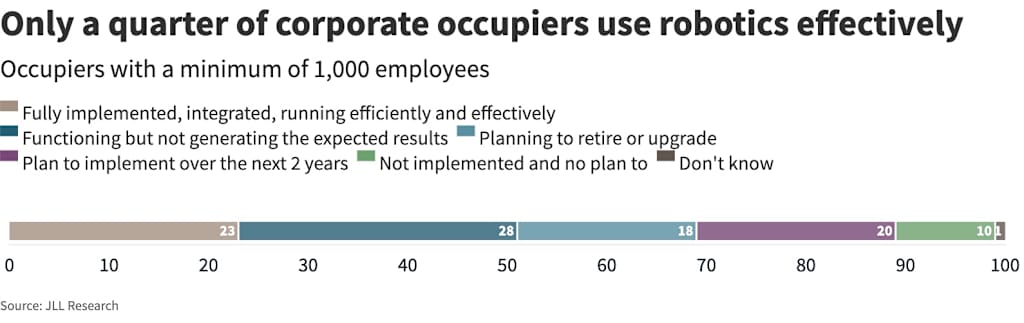

While traditional robots have supported commercial real estate operations for years—handling construction, cleaning, maintenance, and inspections—their success has been moderate. JLL’s 2025 Global Technology Survey reveals that although 69% of large corporate occupiers have adopted these conventional machines, only 23% report full integration with efficient operations. Another 28% describe their robots as functional but not generating expected results, ranking robotics among the lowest in user satisfaction compared to other property technologies such as occupancy management tools and capital planning tools.

Example use cases of robotics in real estate

| Application | Product Example | |

| Construction | Site surveying, drywall, drilling | Canvas 2000CX by Canvas Construction is worker-operated to assist with interior finishing by installing drywall; Also Kewazo developed lifting robots, and other relevant areas include drones and robotic bulldozers. |

| Operations automation | Mail delivery, warehouse robots, smart plugs, and appliances | Physical AI is pushing forward automated package delivery. FieldAI’s Field Foundation Model uses a quadruped from Boston Dynamics to navigate front gardens and stairs to deliver parcels. |

| Inspections & Checks | HVAC systems, boilers, air quality monitoring | Gecko Robotics developed flying drones and crawling robots to detect early issues in critical infrastructure of power and manufacturing plants. |

| Cleaning & Maintenance | Cleaning (windows, floors), repair | With AI and a robotic arm, Skyline Robotics developed a window cleaning robot in use today, while Lucid Bots uses a drone for exterior cleaning. Peppermint Robotics and Peanut Robotics are getting traction cleaning floors and surfaces. |

| Security & Safety | Perimeter patrolling, automated guest check-in | Autonomous security robots like Knightscope’s K5, and Sunflower Labs patrol indoor and outdoor areas and records surveillance footage. |

Robotics breakthroughs

The game-changer is the emergence of “physical AI.” The robotics industry is shooting ahead with the fusion of robotic body, AI powered brain, and integration into context systems. Physical AI enables autonomous decision-making, adaptive behavior, and contextual understanding. Unlike their predecessors that follow programmed routines, these AI-powered systems can learn, adapt, and respond to complex real-world scenarios. This represents a shift from mechanical automation to intelligent physical agents that integrate into enterprise systems to act with context and institutional knowledge, enabling robots to operate in much more sophisticated environments.

However, this is still very nascent for real estate users, as only about 15% of real estate companies reported in 2025 that they have engaged with physical AI-level robotics.

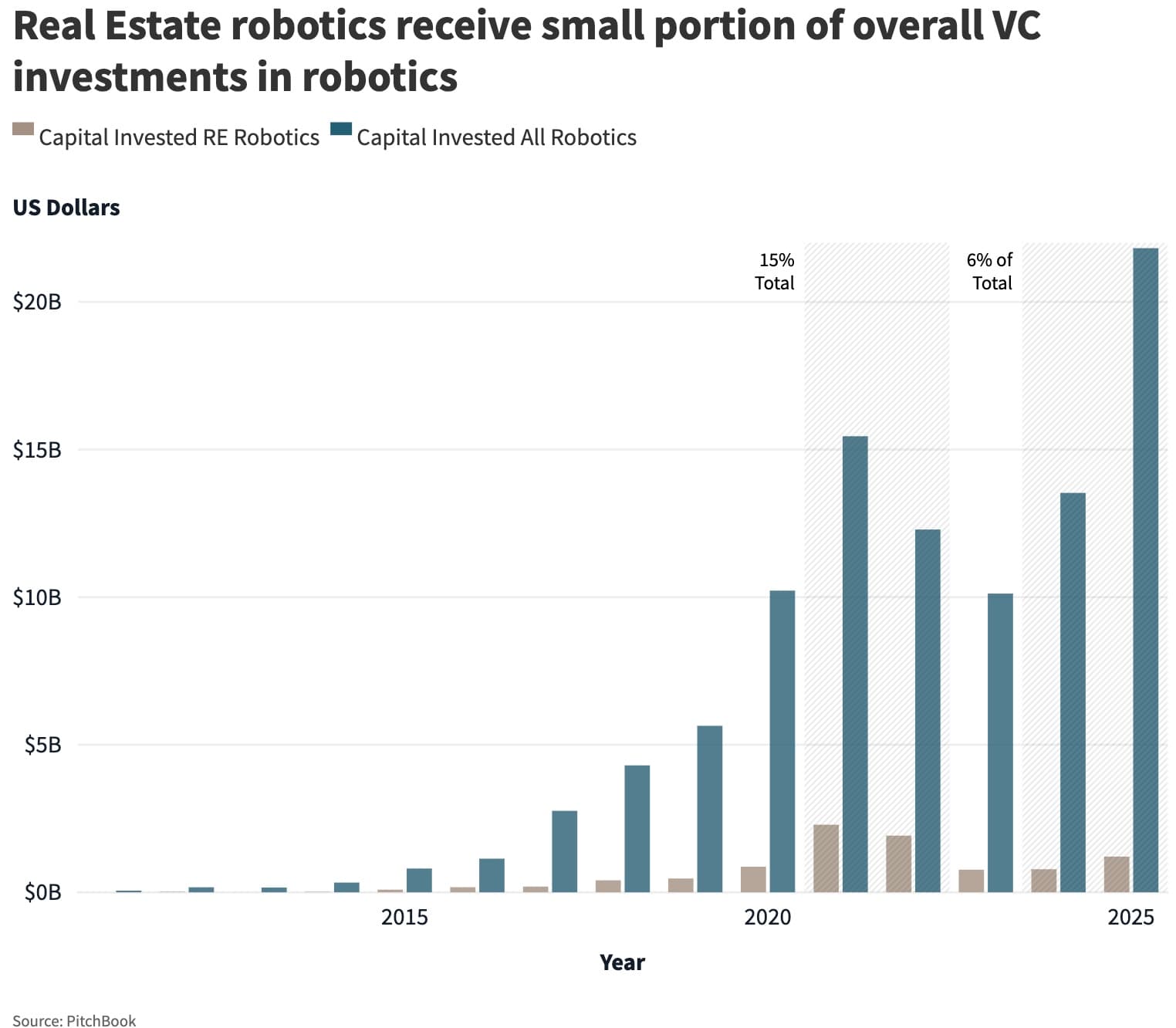

This could soon change because of intensive technology investment. Capital invested in robotics for CRE use cases fluctuates around USD 1 billion, which made up approximately 6% of robotics VC investment last year. This year, over USD 20 billion venture capital funding is flowing into robotics, projected to exceed 2024, according to PitchBook. Although current VC robotics investments are heavily focused on consumer, logistics, and security sectors, these technology developments are also quickly transferring to CRE use cases.

For example, the autonomous cleaning robots market alone was valued at USD 3.45 billion in 2024 and is projected to reach USD 12.08 billion by 2033, growing at a CAGR of 15.2%.

Robot types

| Type | Description | Mobile vs Fixed | Uses |

| Autonomous Mobile Robots (AMR) | Move around environment freely | Mobile | Delivering parcels, security monitoring |

| Automated Guided Vehicles (AGV) | Controlled paths or tracks | Mobile | Warehouse/ factory |

| Articulated Robots | Functions as a human arm | Fixed | Welding, packaging, handling |

| SCARA Robots | Selective Compliance Articulated Robot Arm | Fixed | Fast, precise movements in manufacturing (ie. automotives) |

| Humanoids | Subset of AMR, however in a human-like form | Mobile | Social tasks such as greet guests and offer directions |

| Cobots | Work alongside and share workload of humans to make their work less dangerous or manual | Fixed | Medical surgery |

| Drones | Flying devices that can be autonomous or human controlled | Mobile | Surveying |

Source: Types of Robots and Industry Use of Robotics Technology–Intel

We believe that the AI-powered brain is a critical component of the overall robotic architecture. This concept of orchestration uses AI platforms to control, monitor, and triage incidents within the AI. As robots advance, the coordination and control of a heterogeneous fleet grow in complexity. Orchestration platforms use performance data and camera footage from robots to investigate and flag issues to free up human time, reduce hard tasks, and increase overall productivity.

The robotics orchestration layer serves as a centralized data aggregation platform, collecting information from entire robotic fleets to deliver comprehensive insights and analytics through a unified dashboard interface. By integrating with backend systems such as Integrated Workplace Management Systems (IWMS) like JLL’s Corrigo or Prism, the orchestration layer can autonomously execute work orders and complete the operational cycle by automatically generating and submitting completion reports back to the backend system.

This integration capability transforms robotics from isolated tools into seamlessly connected components of the broader facility management ecosystem, enabling end-to-end workflow automation and enhanced operational visibility across all robotic assets.

Conditions for the robotics adoption tipping point

With the brain of robots getting much smarter, real estate users realize that now we are talking about something fundamentally different from the traditional machines, which raises a critical question for the industry: Has real estate finally reached the long-anticipated tipping point where robots transition from specialized tools to integral operational partners?

The real estate user’s procurement plan is very much grounded on matured, specialized robots that can deliver ROI immediately, rather than investing in untested technologies to gain the innovators advantage as providers. This innovation competition includes the recent race of general purpose humanoids, led by Tesla, Figure AI, and Agility Robotics, which are still teetering on semi-successful pilots, as referenced in JLL’s research How Humanoid Robots Could Reshape Work.

The determining factor for scaled robotics adoption in commercial real estate is a very practical one: Is it more cost-efficient to rely on robots than humans?

The equation is not simply about replacing humans with robots in the exact same workflows doing the same tasks. It is about if robots can justify their cost by providing better outcomes, for example, through enabling new workflows or collecting better data to support decision making . In the JLL Global Tech Survey, both occupiers and investors have reported that data-related workflows are their priority areas for AI pilots. This is an area where robotics have visible advantages.

In these new use cases, the conditions determining whether the tipping point have been reached can be summarized into three categories:

- Technology maturity of both robotics and real estate users

- The business model (for suppliers) and cost structure (for users) for adopting robots

- Macro context regarding labor, regulations, and safety

These factors can vary by markets and even by company.

Are these conditions met for your company?

Depending on the technology maturity for your use case, your company’s cost structure, and the macro context of your business market, your company may be in a promising position to adopt robots.

Product maturity & specifications

The technological breakthroughs might have advanced robots to match your needs. Technology pilots allow companies to capture and collect data that is integral to training and improving the AI that drive the robots. The following aspects have developed rapidly:

- Hardware advancement – Improved sensors, motors, batteries, and key functional units (ie. cleaning hardware) are pushing forward the capabilities of robots. They are now able to navigate more intricate spaces such as offices instead of only large flat floorplans.

- Operating systems & orchestration – Software platforms can integrate robots into existing task and ticketing systems, set schedules, and monitor performance.

- Billing scheme – The industry is moving towards a Robots-as-a-service (RaaS) model, reducing the upfront capital costs needed for customers and including maintenance services.

- Costs – As batteries and hardware become cheaper, the complexity and service required can grow more expensive. Buildings may need to be retrofitted or reconfigured to include charging stations or accommodate robots.

Integration into business

From the JLL Global Tech Survey, corporate technology budgets for the next three years are set to increase and focus on AI. There is a rising interest in robotics, but budget is not yet being allocated.

If considering a pilot, watch out for integration and implementation hurdles within the business. The following factors need to be answered before adoption:

- Implications for the real estate team – Overseeing a fleet of robots might require a new facilitator or data manager role.

- Tolerance for risk – As an emerging technology, the ability to take on the risk varies by organization.

- Infrastructure requirements – One thing preventing scalability of robots is variation in building structures and design. Buildings may change over time to allow robots to operate optimally. Today, one needs to consider compatibility of buildings, such as facade compatibility with window cleaning robots or if charging stations are needed.

- Workflow integration – Many robots can augment the work of humans rather than fully replace their work, so robots will need to integrate into the team dynamic, complete tasks, and participate in feedback loops.

Macro context

Each market and region will have varying factors that impact the return on investment. These factors would be:

- Regulations and compliance – Requirements vary by country and can span from data privacy to labor laws.

- Labor shortage & labor cost – Aging populations and labor shortages have been incentivizing the use of robots.

- Safety – Depending on the sector, using a robot to execute a dangerous task might greatly expand the project scope to include functions that could not be completed by a human, or it reduces insurance needs.

Decide for yourself if these conditions are met for your company and operations. The tipping point varies based on the qualitative and quantitative returns and cost of investment.

Looking into the Future

We believe robotics will gain traction starting in 2026, and we are bullish on the sector’s prospects for commercial real estate. The convergence of physical AI capabilities, substantial venture capital investment, and sophisticated orchestration platforms is creating the foundation for a transformational breakthrough in robotics applications.

While our Global Tech Survey indicates the real estate industry has historically been cautious with new technology adoption, we’re witnessing a fundamental shift in market dynamics. The rapid advancement of AI is unlocking previously unattainable use cases and dramatically improving the viability of robotic solutions for real estate environments. This technological evolution is reducing deployment barriers and making robotics more accessible and practical for commercial applications.

Client sentiment has shifted markedly toward embracing robotic solutions. We’re seeing increased interest among JLL clients to move beyond theoretical discussions and begin active testing of robotic technologies. This growing willingness to experiment represents a critical inflection point for the sector.

We anticipate a significant uptick in pilot programs throughout 2026, with sanitization and security applications leading the charge. These use cases align well with current operational priorities that make them attractive for initial testing grounds. The combination of proven AI capabilities, client readiness, and practical applications positions robotics for growth in the commercial real estate sector.

This convergence of technological capability and market demand creates a compelling investment thesis for robotics in commercial real estate, making 2026 a pivotal year for sector adoption.

Written by Yuehan Wang and Christine Langston, JLL Global Research

For more built world technology insights, subscribe to our newsletter Spark Notes. Interested in a strategic partnership with JLL Spark? Apply for an investment here.